Interest Rate Caps Floors And Collars

An Introduction To Caps Floors Collars Swaps And Swaptions Lancaster Pollard

Difference Between Derivatives Market Finance Investing Investing

How Interest Rate Collars Work Finance Train

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

Interest Rate Caps And Floors Valuation Finpricing

The premium for an interest rate collar also depends on the rollover frequency and how you make your premium payments.

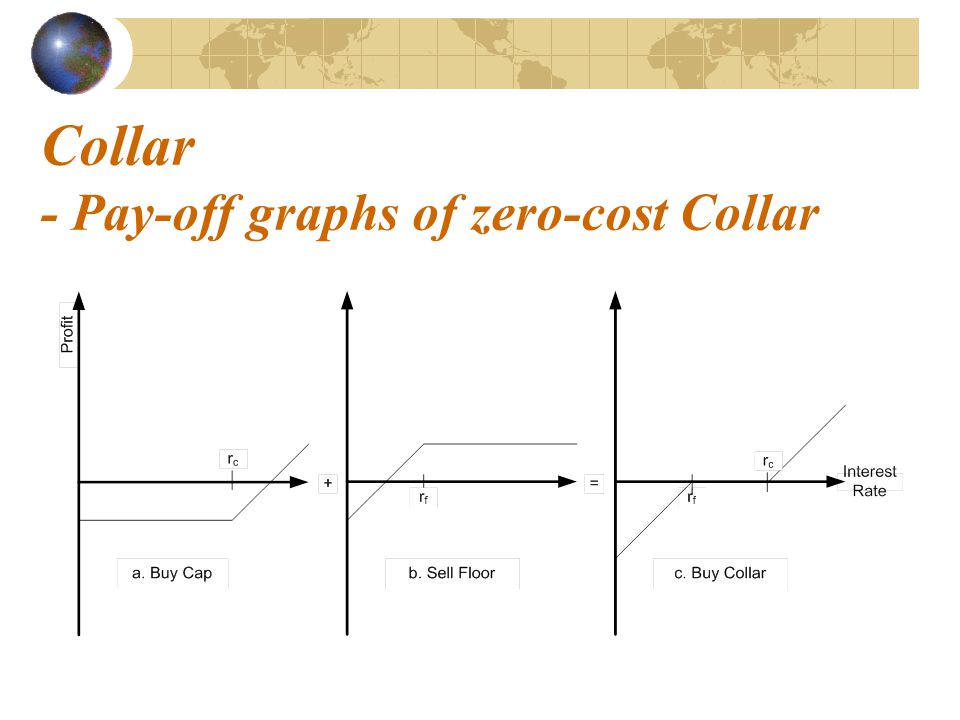

Interest rate caps floors and collars.

Using Caps And Floors Support Center

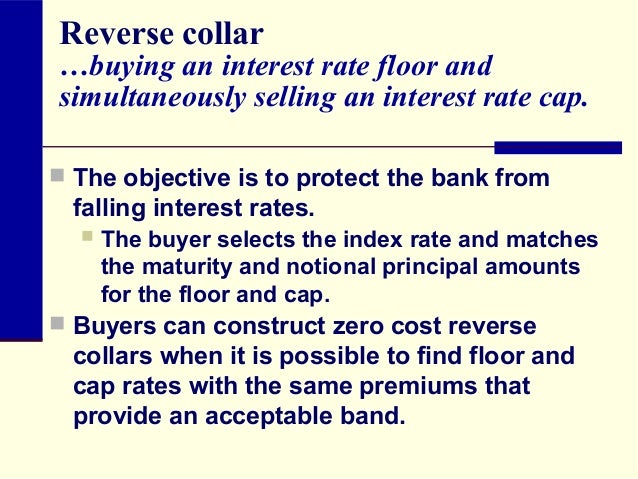

Caps Floors And Collars Ppt Download

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

Interest Rate Collar Definition

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Derivative Market Being An Important Aspect In The Share Market Can Now Be Traded In Online Religare Online Derivatives Market Teacher Life Online Trading

Options Caps Floors

House Plan 3125 00013 Modern Farmhouse Plan 2 556 Square Feet 3 4 Bedrooms 4 Bathrooms Modern Farmhouse Plans Farmhouse Plans House Plans

Dad Hat Or Dad Cap Template Dad Hats Dad Caps Hats

Pin By Joe Mcfarland On Machine Shop Interesting Drawings Blueprints Technical Drawing

Cece Marrakesh Lace Ditsy Print Ruffle Cap Sleeve Top Floral Ruffle Top Bohemian Shirts Cap Sleeve Top

Dog Training A Great Dog Training Tip Is To Make Sure You Understand Other Dogs Are Present When You Puppy Socialization Service Dog Training Puppy Checklist

Via Milavdripclub Air Jordan 1 Low Sb Unc In 2020 Sneaker Outfits Women Red Sneakers Outfit Cap Outfits For Women

Pin By Rebecca Welch On Things Cheongsam Fashion Vocabulary Qipao

Letsfit Fitness Tracker Hr Heart Rate Monitor Watch Ip67 Waterproof Pedometer Watch Sleep Monitor Step Counter T Tracker Fitness Montre Connectee High Tech

N95 Medical Mask 10 Pcs Ship To Usa Face Maskes Kn95mask In 2020 Medical Masks Medical Mask For Kids

Cbk Boss Says Interest Rates Capping Bad For Economy Commercial Bank Interest Rates Boss

Heart Rate Monitors For Physical Education Interactive Health Technologies Heart Rate Wellness Solutions For Schools Smart Watch Personalized Learning Health Technology

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctxj El7gmhrr0f4kolicj0afo1vur0onjiq7yadlp2cs2mkux5 Usqp Cau

Rustic Heart Id Name Badge Holder Retractable Reel Bottle Cap Bottle Cap Is Great For Waist Or Lanyard Usage No Al Id Badge Holders Badge Holders Bottle Cap

A Man A Photo And The Search To Find The Person In It Si Com Humans Of New York New York Photos Person

Lightweight Plaid Bomber Jacket With Collar In 2020 Bomber Jacket Plaid Jackets

Breastfeeding Guidance Medela Breastfeeding Breastfeeding Info Baby Breastfeeding

Holmesbrew Steampunk Keezer With Collar Very Cool Design For Holding Drip Tray Home Brewery Home Brew Supplies Kegerator Diy

Source : pinterest.com